Market Overview

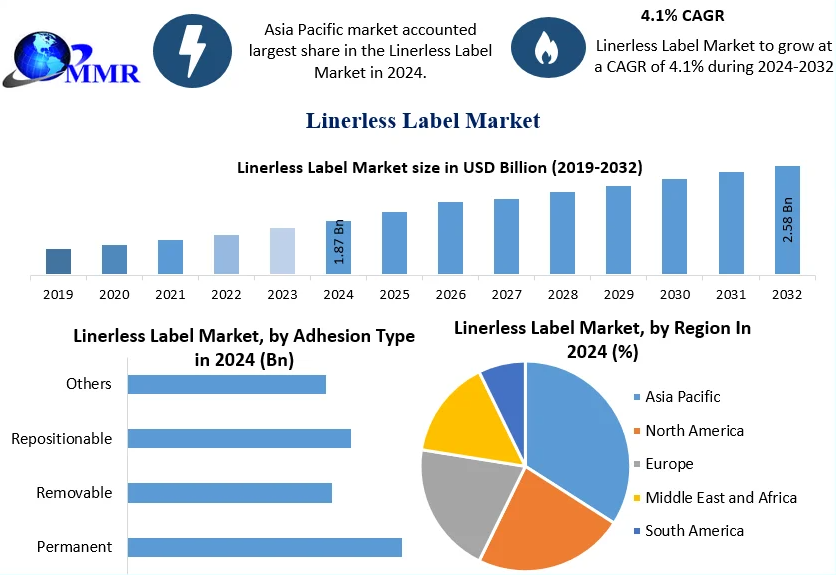

The Global Linerless Label Market was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 2.58 billion by 2032, growing at a CAGR of 4.1% during the forecast period (2025–2032).

Linerless labels, which lack a backing liner and adhere with pressure, have gained significant traction due to their sustainability, cost-efficiency, and waste reduction benefits. These labels eliminate the need for a release liner, reducing material consumption, waste generation, and carbon emissions. Their rising adoption across food & beverage, logistics, and retail sectors positions them as an eco-friendly alternative in modern labeling and packaging applications.

Gain Valuable Insights – Request Your Complimentary Sample Now @ https://www.maximizemarketresearch.com/request-sample/122602/

Market Size and Growth Projections

-

Market Value (2024): USD 1.87 Billion

-

Forecast Value (2032): USD 2.58 Billion

-

CAGR (2025–2032): 4.1%

The market’s expansion is fueled by increasing environmental regulations, the global shift toward sustainable packaging, and the rapid growth of e-commerce and FMCG sectors. The rising use of smart labeling technologies and automation in packaging lines is expected to further support demand growth globally.

Key Market Drivers

a. Sustainability and Waste Reduction

Growing emphasis on eco-friendly packaging is a primary driver. Linerless labels reduce raw material use, waste disposal, and CO₂ emissions — aligning with global sustainability goals and circular economy principles.

b. Increasing E-commerce Penetration

The boom in online retail and logistics has created substantial demand for efficient, durable, and cost-effective labeling solutions. Linerless labels enable quick, reliable labeling for parcels and shipment tracking.

c. Expansion of the Food & Beverage Sector

Food safety, product differentiation, and branding rely heavily on labeling. As packaged and ready-to-eat food demand rises—especially in Asia-Pacific—linerless labels are increasingly adopted due to their versatility and compliance with food contact standards.

d. Cost and Operational Efficiency

Eliminating liners reduces not only raw material costs but also storage, transport, and labor expenses, enhancing overall production efficiency for manufacturers.

Feel free to request a complimentary sample copy or view a summary of the report: https://www.maximizemarketresearch.com/request-sample/122602/

Market Restraints

-

Design Limitations: Manufacturers face challenges in creating labels of non-standard shapes or complex designs, restricting use in premium or customized branding.

-

High Raw Material Costs: Fluctuations in adhesive and facestock material prices can impact profitability.

-

Limited Awareness: In certain emerging economies, lack of awareness about linerless labeling technology hampers adoption.

Market Segmentation

By Component

-

Facestock (Dominant Segment): Accounts for the largest share due to its critical role in print quality and brand representation. Emerging materials like vellum, sugarcane, and metalized papers are enhancing label performance and sustainability.

By Adhesion Type

-

Repositionable Labels: Expected to grow rapidly owing to flexibility in application.

-

Permanent Labels: Currently dominate in volume, particularly in retail and logistics sectors.

By Printing Technology

-

Flexographic Printing: Holds the largest share due to speed, flexibility, and cost efficiency.

-

Digital Printing: Gaining traction for short-run and customized labeling solutions.

By Printing Ink

-

Water-Based Ink: Leads the market due to compliance with environmental standards and low VOC emissions.

By Application

-

Food & Beverage: Largest end-use segment, driven by the growth of packaged food, retail, and convenience product markets.

-

Pharmaceutical & Personal Care: Increasing adoption for traceability and regulatory compliance.

-

Retail & Logistics: Growth driven by the e-commerce boom and automation in packaging lines.

Dive deeper into the market dynamics and future outlook: https://www.maximizemarketresearch.com/request-sample/122602/

Regional Insights

Asia-Pacific (Dominant Region)

-

Expected to hold the largest share, supported by rapid industrialization, urbanization, and expansion of the food & beverage and logistics industries in India, China, and Southeast Asia.

-

Strong government emphasis on sustainability initiatives further supports market growth.

North America

-

Mature market with a well-established retail and logistics infrastructure. Growth is steady, driven by high adoption of smart and sustainable labeling solutions.

Europe

-

Growth supported by stringent environmental regulations and the presence of major packaging manufacturers. Increasing demand from pharmaceutical and personal care sectors contributes to steady expansion.

Middle East, Africa, and South America

-

Emerging opportunities due to expanding retail networks, increasing food exports, and gradual adoption of green labeling solutions.

Key Industry Developments

-

RR Donnelley & Sons Company (2021): Expanded linerless label production capabilities to improve efficiency.

-

Coveris Acquisition of Amberley Labels (2021): Strengthened its self-adhesive labeling portfolio in Europe.

-

Herma (2021): Introduced the eco-friendly inNo-Liner device with proprietary adhesive technology.

-

Lexit Group (2021): Added a new coating line to enhance European production capacity.

-

Bostik (2021): Launched new adhesives for sustainable quick-service restaurant packaging.

-

Ritrama & ABInBev Collaboration: Adoption of Core Linerless Solutions (CLS) for beer labeling, highlighting growing industrial application.

Competitive Landscape

The global market is moderately fragmented, with key players focusing on innovation, capacity expansion, and sustainability to strengthen market presence.

Major Players Include:

-

Coveris

-

Avery Dennison Corporation

-

Lexit Group AS

-

Hub Labels

-

Bostik

-

Ravenwood Packaging

-

Innovia Films

-

Constantia Flexibles

-

Reflex Labels Ltd.

-

Weber Packaging Solutions

These companies are investing in eco-friendly adhesives, automation technologies, and advanced printing solutions to maintain a competitive edge.

Conclusion

The Global Linerless Label Market is on a steady growth trajectory, driven by rising environmental awareness, cost advantages, and expanding end-use industries. As companies across the globe push toward sustainable packaging solutions, linerless labels are emerging as a key innovation in the labeling landscape.

Asia-Pacific remains the primary growth engine, while technological advancements in printing and adhesive formulations are expected to unlock new opportunities globally. Despite design limitations and raw material price volatility, the market’s long-term outlook is positive, underpinned by the packaging sector’s green transformation.

More Related Reports

India Edible Oils Market https://www.maximizemarketresearch.com/market-report/india-edible-oils-market/125654/

India Chocolate Market https://www.maximizemarketresearch.com/market-report/india-chocolate-market/24126/

Hazelnut market https://www.maximizemarketresearch.com/market-report/hazelnut-market/123229/

About Us